Quote California Term Life Plans Across Dozens of Plans and Carriers

How to Run your California Term Life Quote

This is actually one of the easiest products out there but there's so much pressure sales out there, people feel confused and get turned around.

We're going to break it down for you here and show you exactly how easy it can be!

First, our credentials:

This is what we'll cover:

- Why term life insurance

- What to decide before quoting term life

- How to quote term life insurance

- Health and term life rates

- Picking the best term life carrier and plan

Let's get started!

Why term life insurance

The first big source of confusion is around the type of life insurance.

There are really two types out there:

- Term life insurance

- "Permanent" life insurance (generally whole or universal life)

Think renting versus owning but with a huge difference...cost!

For most true life insurance needs, term life is the way to go. Outside of odd tax planning situations, it's hard to justify the cost of whole life insurance.

Meaning, unless you're Jeff Bezos and you're want to take out a massive whole life policy that's tax deductible to a company and then borrow against it, whole life is super (SUPER) expensive for what it is.

As investment, you're so much better going with the market or even annuities!

Okay…that's our 2 cents. If you really need life insurance, Term life is super cheap and fits the bill 99% of the time.

Basically, we need to provide income or an immediate asset in case we pass away to support those that are dependent on us financially!

That's it!

- Get kids into adulthood

- Pay off mortgage, bills, etc

- Support loved-one financially

- Address loss in a key business role

If you're shopping life insurance, we're not telling you anything you don't already know. You have your very own, personal reasons to get life insurance.

Look…life insurance companies and agents make a lot of money off of whole/universal life insurance so get ready for the full court press.

If you REALLY want whole life, we can quote it for you. It just doesn't make sense for most people and yet…that's what they're getting pitched.

Not here!

Okay, so before we jump into the quote process, what do we want to decide on first?

What to decide before quoting term life

It's pretty simple.

We want to decide on the following (at least as a rough sketch):

- How long do we want to protect in terms of time

- How much term life we need

- Do any "riders" make sense?

The first two are really the crux of the matter.

First, term life insurance is fixed for a period of time. Then it…"terms" or ends.

It's generally 5, 10, 15, 20, 25, 30 increments but there are all kinds of options out there.

So…if I have a new born, I probably want 25-30 years of term life. Sure, you can get them out to age 18 but as a father of a 22 and 24 year old, let me just say…it might be longer than you think!

A 30 year mortgage is easy. 30 years.

Covering your role in a business?? That's trickier. We're trying to get past the point where that income stream is "needed". If you're in your 50's, that might only be 15 years.

We can run multiple periods of time (15, 20, 25 years for example) so you can see the price difference.

General rule of thumb…the longer the period of time, the more expensive the same amount of coverage per year.

But…depending on your age and health, the difference may not be much between 15 and 20 years and that extra five years might make a huge difference.

It's always cheapest to buy term life insurance RIGHT NOW versus years from now so going longer as a buffer is smart.

We're happy to walk through any questions on this front but quote different term periods of time.

Next up…amount of term life coverage.

This is the other big question.

How much term life coverage?

We can quote different amounts as well ($100K, $250K, $500K, etc).

Amounts can start in low 10's of thousands (usually called final expense to cover funeral charges and pay off debts) up to millions.

We have customers that apply for millions of term life generally around business needs.

Everyone's situation is unique and no need is unimportant!

You'll also notice that the price difference between two levels may not be that big of a difference so make sure to run your ideal amount plus up or down from there.

Our one recommendation is to err on the upside since the cost per $1000 of term life is so cheap and it will never be cheaper as we get older.

What about all the "bells and whistles" or riders available.

We're not big fans of riders. Riders are generally just a great way to add "margin" to a life insurance policy for the carrier. There…we said it.

Term life coverage itself is an essential tool and it's priced very well. It makes more sense to just get a longer term at a high amount for the cost difference of the rider.

The core term life product is very cheap per $1000 of coverage. Why muddy the water and make it more expensive.

Life insurance companies are not going to add in benefits that don't pencil out financially to their bottom line!

We're happy to investigate different riders but focus on maximizing your protection (both amount and length) first.

Okay…so how do we quote!

How to quote term life insurance

This is super easy! We just need the basic information above and we're off to the races.

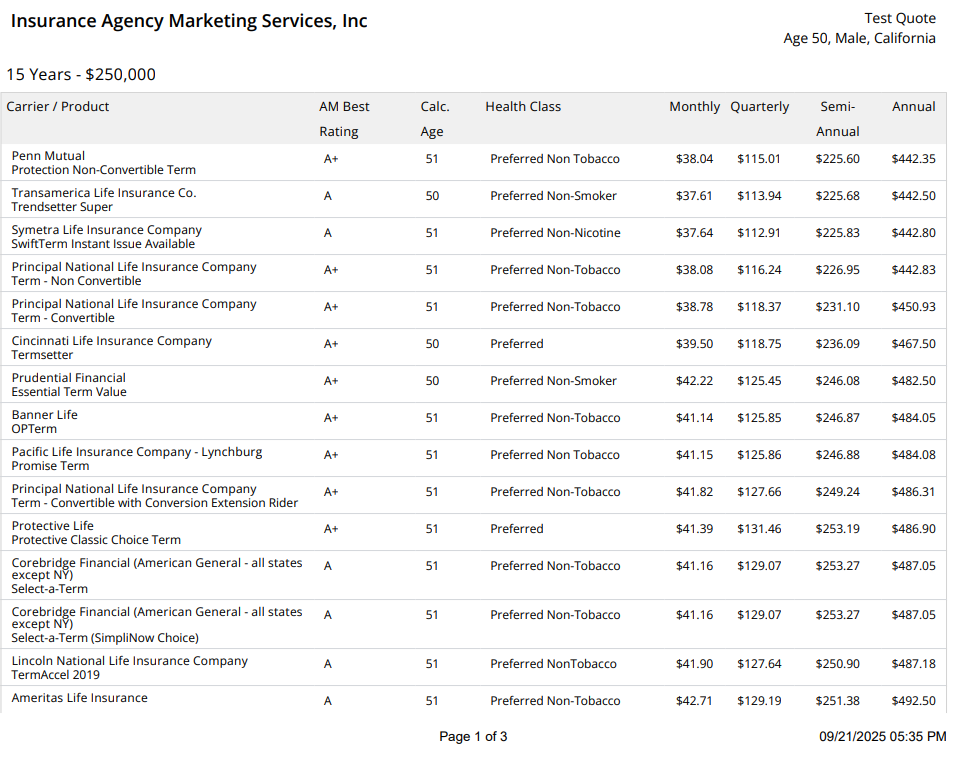

We quote all the major carriers and the simple report (sample below) will sort them by cost, term length, and amount!

It couldn't be easier! You'll receive something like this but based on

your info and requirements:

If the rating for the carrier solid (A or better), go with the cheapest option available since term life insurance is really a commodity these days.

Once you've decided on the right carrier and plan, we can start the online application for you on this side. It's all online now!

We do not push, sell, or even reach out to you unless you have questions! Check out the Google ratings. It's just how we do business as agents and the rates to are identical through us, direct with the carrier, or with any other agent.

The difference is that we can help you through the entire process and help you navigate… the next section!

Health and term life rates

Unless you're in spotless health (almost no one these days), this is the one piece we can really help with.

Term life insurance is medically underwritten.

They can change rates and even decline based on health. Medical information will be requested from your doctors and a paramedical exam will likely be needed.

It's not too bad..they schedule to come to you and handle the whole process.

That being said, different carriers can be more flexible depending on your health status and it really varies by issue and history.

This may be our biggest advantage to you in that we can pre-check the market for your situation to see who is more likely to offer the best rate.

We can also let you know if there are guaranteed issue (simple underwriting) options in case of big health issues.

Reach out to us or simply request your term life quote above to get started! Always happy to pick a time to chat as well!